The Importance of Financial Education in Families: A Path to a More Secure Future

For a long time, the subject of “money” was avoided at home. Many families prefer not to discuss finances out of fear, shame, or because they think it is not a subject for children.

Advertising

But the reality is different: the sooner we start talking about money at home, the better prepared we will be to deal with it throughout our lives.

School teaches, but the example comes from home

Advertising

School may teach math, history, and science, but it rarely teaches how to manage a salary, pay bills, or plan a major purchase.

This role must come from the family. It doesn’t matter if you earn a lot or a little. Teaching how to use what you have well is essential.

Advertising

Money is behavior, not just numbers

Let’s think about it together: how many times have you seen someone sink into debt because of misusing a credit card? Or commit their entire salary to paying for things that weren’t even that necessary? These behaviors don’t come out of nowhere.

They come from a lack of dialogue and guidance from an early age. When a child grows up in an environment where money is not discussed, they learn on their own — usually in the worst possible way, through trial and error.

Financial education is not about complex formulas. It’s about everyday decisions. It’s about teaching how to make choices, understand priorities, and avoid the impulse to spend without thinking.

It’s about showing that money is a tool, not the ultimate goal.

What happens when you don’t talk about it?

When the subject is avoided, children learn on their own — usually through pain. Credit card debt, poorly planned financing, and lack of control become part of the routine.

What was missing? Dialogue, guidance, and, above all, example.

The value of money and the value of effort

A valuable lesson is to teach that money does not “appear” on the card. It is the result of effort, work, and time invested.

When children understand this, they value each purchase much more and begin to consume more consciously.

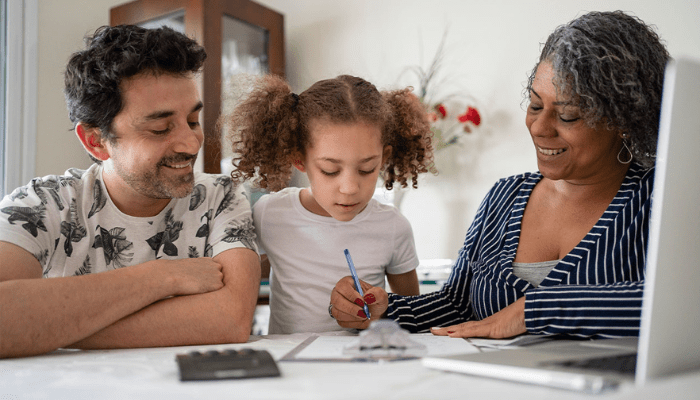

Family planning: everyone can participate

Planning finances doesn’t have to be something only adults do. Children and teenagers can (and should) participate in decisions, in a way that is appropriate for their age.

Get everyone to think together: how can we save energy? How can we save up for a trip? How can we cut unnecessary expenses?

And for those who already have teenage or adult children, it’s never too late to start this dialogue. Talking about financial education can even strengthen family ties. It can be an opportunity to learn together, support each other, and perhaps even resolve old debts or problems that remained unsolved precisely because of a lack of conversation.

In the long run, the impact of this is enormous. Families who talk openly about money, who plan together, who build common goals and objectives, are better able to deal with unforeseen events, save for the future, and even realize their dreams with greater security. This creates a healthier relationship with money and, consequently, a more balanced life.

Allowance: a practical lesson in financial education

Allowance is a powerful tool. More than just giving money, it gives autonomy and responsibility.

If a child spends everything in one day, they learn that they need to manage their money better next time. It’s a mistake that teaches them a lesson without causing major damage.

What is the best age to talk about finances?

The best age to start talking about finances is earlier than many people think. From the age of 4 or 5, children are already able to understand basic concepts such as exchange, value, and choice. At this stage, it is possible to introduce simple notions—such as the fact that money is limited and that sometimes you have to choose between one thing and another.

As they grow older, these lessons can be expanded to include topics such as economics, planning, and even saving. The key is to adapt the language to their age and make learning natural, using examples from everyday life.

The earlier children are included in these types of conversations, the greater their ability to make informed decisions in the future. Financial education is an ongoing process — and it starts in childhood.

Example is worth more than any advice

There’s no point in asking children to save if their parents spend impulsively or live on overdraft.

And it’s worth remembering: teaching financial education at home does not require advanced technical knowledge. You don’t need to be an economist, let alone an investment expert.

Just speak clearly, truthfully, and with a little patience. Show them how things work. Show them what is a priority. Show them that money can—and should—be used purposefully.

Actions speak louder than words. If you want your children to grow up with good financial habits, start by modeling those habits in your daily life.

It’s never too late to start

Even with teenage or adult children, financial dialogue is still possible. Take advantage of moments of conversation to share lessons learned, mistakes, and strategies.

Talking about money can even bring the family closer together and create a climate of cooperation.

The benefits of a financially conscious family

Families that organize together are better able to deal with the unexpected, plan for the future with greater clarity, and achieve their dreams with greater security.

Unity around the topic of “money” strengthens bonds and brings greater peace of mind for everyone.

How to get started in practice?

Here are some simple and effective tips to start this process at home:

- Set up a family budget with all members.

- Set financial goals as a group.

- Encourage the habit of saving.

- Talk openly about financial mistakes—and what was learned from them.

- Show the value of the effort involved in each achievement.

Another essential point is to teach the value of money. Not the numerical value, but the value of effort. When a child understands that a new toy represents hours of work, they begin to see money as a consequence of dedication, and not just as something that “appears” on a card. This type of learning creates more responsible, conscious adults who are prepared to deal with reality.

Conclusion: investing in financial education is investing in the family

Financial education is not a luxury for those who have money to spare. It is a necessity for any family seeking security, balance, and freedom.

And it all starts with a conversation. An attitude. An example.

If this content has helped you in any way, subscribe to the channel, leave your like, and share it with someone you love. Together, we can transform the way families deal with money. See you in the next video!